lead

Direct Tax

Hany Elnaggar examines how the OECD’s global minimum tax is reshaping the GCC’s investment incentive landscape, shifting the region from rate-based competition toward substance-driven economic positioning

May 27, 2026

features sponsored features special focus local insights

-

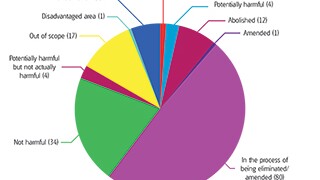

BEPS Action 5 – Countering harmful tax practices more effectively by taking into account transparency and substance is one of the four BEPS minimum standards. To date, 102 jurisdictions have committed to its implementation, and 2017 is a decisive year in translating that commitment into action. Achim Pross, Kevin Shoom and Melissa Dejong of the OECD, discuss the first results of the work under BEPS Action 5, and its significance in achieving the goals of the BEPS project.

BEPS Action 5 – Countering harmful tax practices more effectively by taking into account transparency and substance is one of the four BEPS minimum standards. To date, 102 jurisdictions have committed to its implementation, and 2017 is a decisive year in translating that commitment into action. Achim Pross, Kevin Shoom and Melissa Dejong of the OECD, discuss the first results of the work under BEPS Action 5, and its significance in achieving the goals of the BEPS project. -

With the CCCTB back on the EU agenda, Richard Murphy, professor of practice in international political economy at City, University of London, argues it does not represent true consolidation and could fail in its objectives.

-

The OECD has continued to evaluate and work on refining its transfer pricing guidelines regarding several BEPS initiatives, write David Jarczyk and John Wiora of ktMINE.

Sponsored Features

-

Sponsored by KNAV IndiaIndia’s transfer pricing overhaul expands safe harbours at scale and accelerates advance pricing agreements alongside the statutory recodification of the Income-tax Act, report Uday Ved, Hetav Vasani, and Jainesh Nahar of KNAV

-

Sponsored by insightsoftwareJoin KPMG and insightsoftware on June 25 as ITR presents a free webinar on the evolving role of tax professionals and how technology is driving the transformation

-

Sponsored by DeloitteJess Williams, Jimmy Man, and Olivier Hody of Deloitte explain how tax can be elevated from a post-close support function to a value-realisation tool in M&A transactions through quick wins and longer-term actions

Special Focus

-

Sponsored by YulchonSeveral South Korean transfer pricing cases have established clearer judicial standards emphasising robust comparability analysis and stronger functional and economic evidence. Yulchon tax partners provide practical insights for navigating the heightened requirements

-

Sponsored by RSM IndonesiaIchwan Sukardi and T Qivi Hady Daholi of RSM Indonesia examine how geopolitical conflict and economic volatility are reshaping transfer pricing risk and enforcement, with a particular focus on Southeast Asia and Indonesia

-

Sponsored by Tax PartnerMonika Bieri and Daniel Schönenberger of Tax Partner use a Swiss lens to examine how workforce mobility is reshaping transfer pricing models, and why the location of key decision‑makers is becoming a critical tax risk

Local Insights

-

Sponsored by Lakshmikumaran & SridharanIndia’s Finance Act, 2026 introduces a tax framework for foreign companies using local data centres but leaves several questions unresolved, say S Vasudevan, Prachi Bharadwaj, and Loveena Manaktala of Lakshmikumaran & Sridharan

-

Sponsored by Pérez-LlorcaNicolle Barbetti of Pérez-Llorca explains how the Capitalisation of Companies Incentive has reshaped Portugal’s corporate financing landscape and highlights how binding rulings have clarified key issues in its application

-

Sponsored by PwC ChileNatalia Núñez and Antonia Valdés of PwC Chile analyse the new bill’s tax implications for a key sector, considering the provisions of the Mining Royalty Law