Firm

Rising demand for specialist expertise has fuelled the growth in tax partner headcounts, Cain Dwyer found; in other news, Switzerland has been urged to reconsider pillar two

Trophy assets are evolving from personal indulgences to structured investments, prompting family offices to prioritise tax efficiency, governance discipline, and cross-border compliance

As demand for complex, cross-border private client counsel spikes, Patrick McCormick sees opportunity in starting from scratch

As part of an exclusive global alliance, KPMG will become one of Anthropic’s ‘preferred consultants’ for private equity

Sponsored

Sponsored

-

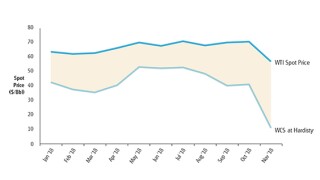

Sponsored by Deloitte Transfer Pricing GlobalVolatile oil markets in 2018 presented significant challenges to Canadian exporters, but a shortage in natural gas production globally presented a complimentary opportunity. Deloitte’s Andreas Ottosson and Markus Navikenas discuss the transfer pricing implications.

Sponsored by Deloitte Transfer Pricing GlobalVolatile oil markets in 2018 presented significant challenges to Canadian exporters, but a shortage in natural gas production globally presented a complimentary opportunity. Deloitte’s Andreas Ottosson and Markus Navikenas discuss the transfer pricing implications. -

Sponsored by Deloitte Transfer Pricing GlobalEnergy companies using an asset-backed trading (ABT) model can hedge against volatile markets by better controlling their supply chain, but this can also trigger new transfer pricing issues. Deloitte’s Nick Pearson-Woodd and Marius Basteviken discuss.

-

Sponsored by Deloitte Transfer Pricing GlobalThe OECD has issued new guidance on applying the profit-split method (PSM) in the energy and resources (E&R) sector. But will this see an uptick in its use? Deloitte’s Mark Barker and Aengus Barry discuss.

Article list (load more 4 col) current tags