|

The technical advances companies went through preparing for E-Bilanz can pay dividends if applied to internal tax calculations |

Here, Andreas Kowallik of Deloitte explores technology-supported tax data analytics, which is the game changer and the key to future success.

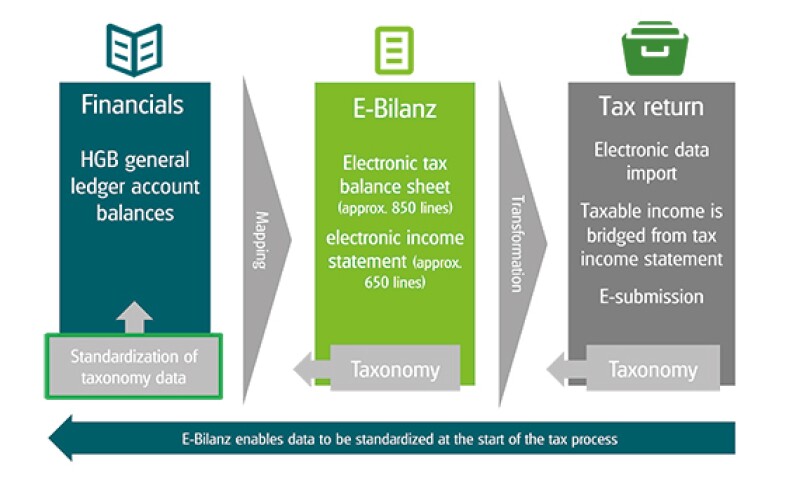

Tax authorities no longer review companies' tax assessments by digging through piles of paper, but analyse them on the basis of bits and bytes. Submitting a fully standardised tax basis balance sheet and tax income statement ("E-Bilanz") in extensible business reporting language (XBRL) in machine-readable format to the German tax authorities has been mandatory for most German companies since the 2013 company tax return (phase 1).

The advantages for the tax authorities are clear: they benefit from a higher degree of automation and lower personnel and administrative costs. Recording errors are now a thing of the past and, thanks to almost unlimited storage capacity, archiving electronic datasets is much less expensive and far more efficient than archiving paper documents.

E-Bilanz: higher data quality and greater legal certainty for companies

Since its introduction three years ago, the E-Bilanz has passed the practice test. The tax authorities have extended the E-Bilanz to all taxpayers that need to submit a tax basis balance sheet and to all partners of partnerships starting from the 2015 tax return (phase 2).

Thanks to the E-Bilanz, the tax authorities now receive completely standardised trial-balance-level datasets once a year from millions of German taxpayers with business income. These datasets include, completely standardised for tax purposes, all general ledger accounts of the balance sheet and the income statement. This data pool is constantly growing and can be electronically analysed (this process is often referred to as "electronic data access light") and allows the German tax authorities to conduct detailed benchmarking-, risk-, time-series-, sector-, industry-, and trend analyses. The tax authorities focus on determining the review depth during the tax assessment and the tax audit by comparing the E-Bilanz to the content of the electronic tax returns and by validating the E-Bilanz data against other electronic data pools. As a result, companies can expect a timely audit and a risk-based case selection. In addition to the data quality of the new process, this entails greater legal certainty and may thus represent an improvement for many tax-audited companies.

Many companies initially viewed the technical upgrade to E-Bilanz with scepticism and reservation. This reluctance was born from high one-off costs, the lack of an overall concept and fear of duplicate data requests. However, its successful launch, the certainty that the E-Bilanz obligations will have to be fulfilled on a regular basis and new software solutions that make the potential of E-Bilanz more palatable to companies have prompted a shift in perspective.

Many companies which had to bear a high technical and organisational burden for the switchover want to benefit from the opportunities offered by the E-Bilanz. According to the FAQ document on E-Bilanz published by the tax authorities, the E-Bilanz offers companies a basis from which to redesign their record-to-report processes for producing tax calculations and tax returns, the opportunity to reduce administration costs thanks to a higher degree of automation, and a faster way of gaining legal certainty.

Integrated processes and automation offer new opportunities

Regarding phase 1, the German tax authorities have not (yet) achieved their transparency and efficiency improvement targets from the E-Bilanz. In response, the state tax authorities of North Rhine-Westphalia and Schleswig-Holstein have already announced they will extend the minimum scope of datasets in phase 2. In autumn 2015, the regional tax office of North Rhine-Westphalia instructed its tax offices to require the submission of additional information to support E-Bilanz datasets. The implications of failure to submit sufficient back-up information will be decided on a case-by-case basis, depending on the facts and circumstances. In the event of a tax audit risk class, missing documents (eg. account details) are to be requested on a regular basis since a viable decision on a tax audit case cannot be made without a minimum level of information; in such cases, a lack of documentation is treated as implying that a tax audit is required. Removal from, or non-inclusion in, the audit plan can only be considered if the tax office can take a desk-review decision on the basis of the provided information.

The E-Bilanz allows companies to integrate their tax calculation and tax return processes even more closely than before and to fully automate them, thereby enabling them to reduce their administrative costs. The mid-term transition to an electronic self-assessment for company income tax returns that has been planned and prepared by the tax authorities. This has been done in conjunction with the elimination of the tax assessment process and tax assessment notices, and will also lead to substantial and permanent reductions in administrative costs.

Until then, all companies should respond proactively to the foreseeable increase in requests from the tax offices regarding their E-Bilanz datasets by continuously improving the data quality, for example by reducing the number of fall-back items in their datasets by using voluntary taxonomy items and by including detailed account information in all datasets. "Nil" values that cannot be objectively, individually condensed mapping directly onto summary fields and the extensive use of fall-back items should be avoided in all E-Bilanz datasets.

Diagram 1: Change in taxation process due to E-Bilanz |

|

Paradigm shift for tax departments: data managers instead of data consumers

Following the often burdensome switchover to the E-Bilanz, companies face a second challenge as the E-Bilanz gives the tax department access to extensive standardised German tax data pool for the first time. This data was previously only available to the accounting department on a similar scale.

In the digital age, future-oriented tax departments are no longer only consumers of finance data and finance information from the accounting systems: they need to become data managers that actively handle, manage, and evaluate tax-sensitive data in accordance with the company's overall strategy in a forward-looking manner. This presents personnel, as well as IT systems, with new challenges. Tax data analytics allows for a high degree of compliance, valid forecasts and the ability to identify savings, leading to organisational restructuring potential. It is therefore a highly effective management tool for all modern tax departments.

|

|

The E-Bilanz allows companies to integrate their tax calculation and tax return processes even more closely than before and to fully automate them |

|

|

All companies should assess their tax audit profile and risk class and verify whether any measures are indicated to attain a better risk rating in terms of the risk management systems, which are being designed and implemented by the German tax authorities. The strategy of some German state tax authorities is to use the E-Bilanz datasets proactively in the future as a basis for risk management and for planning tax audits. The companies in question should take this into account. A better risk rating could give large companies, which are subject to continuous tax audits, preferential access to a timely tax audit. A more favourable risk rating in the case of small and medium-sized companies could mean that they are not tax audited, or are less likely to be tax audited every year.

When performing a technical validation of E-Bilanz datasets in response to the tax authorities' risk management, each company should verify all E-Bilanz datasets in terms of consistency with the related e-tax return and e-tax filings (eg. VAT reconciliation, match the sales from the e-balance sheet against the VAT return).

For larger groups of companies, initial experience has shown that datasets are surprisingly and frequently inconsistent as many (group) tax departments have apparently failed to provide all subsidiaries and all external advisors with a clear strategy for the introduction of the E-Bilanz (ie. initial mapping) and the adjustments to the ongoing accounting processes (ie. mapping of new accounts) as part of the switchover.

These groups should ensure that they not only verify all E-Bilanz datasets for each individual company, but also examine structural consistency and integrity over the entire group and analyse the areas where technical solutions and tools are available. This review and validation often shows that consistency and integrity need to be enhanced by amending or improving the mapping and/or tagging of the general ledger accounts.

Diagram 2: Tax Data Analytics: Deloitte’s E-Bilanz validation reports |

|

Tax 4.0: data management as a success factor of the future

After some initial scepticism, E-Bilanz's reputation in has improved among many companies. A growing number are seeing and understanding the E-Bilanz as an opportunity for process integration, process automation using a record-to-report approach and greater legal certainty, all of which go hand in hand with digitisation to create ideal conditions for proactive data management in accordance with the overall business strategy. IT-supported tax data analytics help facilitate this realignment through a high degree of compliance, valid forecasts and the use of additional savings and organisational potential, which allow the tax department to add value to the overall organisation.

|

|

Andreas KowallikPartner in Munich, Germany Tax management consulting Deloitte Tel: +49 89 29036-8684 Email: akowallik@deloitte.de Andreas Kowallik heads tax management consulting in Germany. His team consists of specialists in tax processes, tax data, tax technology, and tax organisation who support businesses to enable them to meet the challenges of multijurisdictional tax operations by transforming processes and technology to enhance efficiencies, align data, and improve transparency from electronic resource planning (ERP) systems all the way through the reporting and documentation process. Andreas has more than 20 years of work experience serving international clients from different countries and industries on national and cross-border tax matters. He holds a master of business administration degree and a PhD in international taxation. Andreas is a German Certified Tax Adviser. He is a regular lecturer at external conferences and regularly publishes on German taxation both in domestic and international tax journals and publications. In May 2015, International Tax Review – as part of its European Tax Awards 2015 – gave Deloitte Germany the "European Tax Innovator of the Year" award for innovative process consulting and system developments generating efficiency gains for corporate tax departments. |