A webinar hosted by ITR has addressed the question of whether tax functions are doing enough to prepare for the implementation of BEPS pillar two. With the rules effectively already in play, the discussion summarises the key rules, the safe harbours, and the approaches that can be taken to avoid falling behind.

Senior tax professionals from Wolters Kluwer, a global provider of software and knowledge solutions for corporate tax professionals, and BDO, the accountancy and business advisory firm, raise concerns based on their experience and explain what in-scope companies should be prioritising at this stage, and the scenarios they should look to avoid.

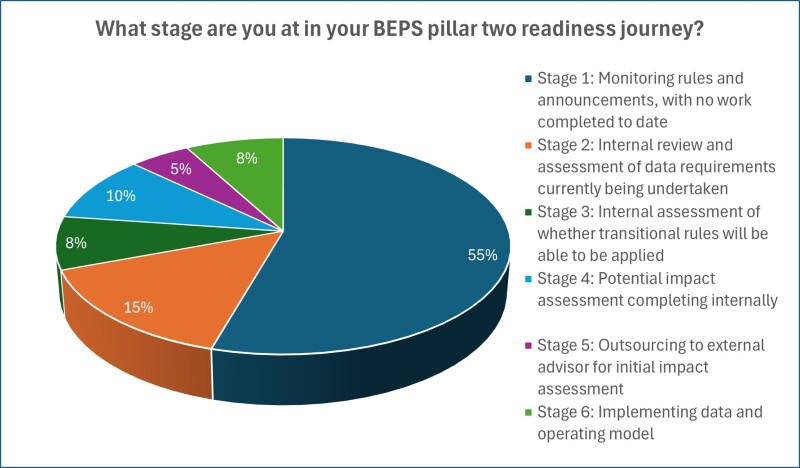

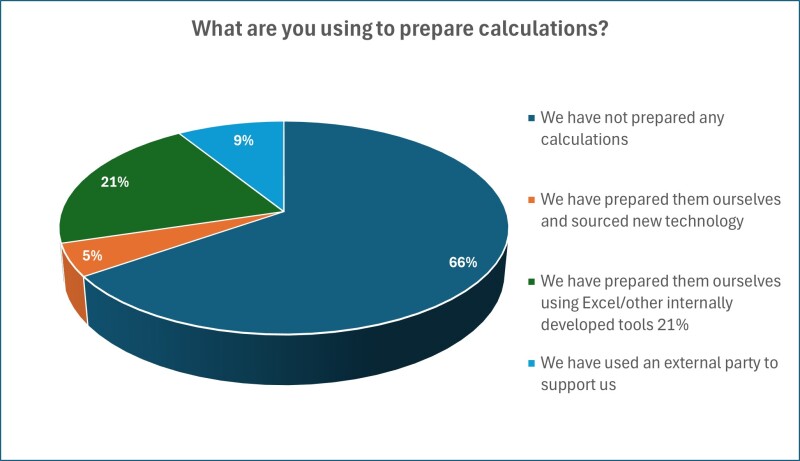

A poll conducted for the webinar suggests there is indeed much to be done with regard to pillar two, with 55% of the respondents saying their organisations are “monitoring rules and announcements, with no work completed to date”, while 66% are yet to prepare any calculations.

The above findings complement a Wolters Kluwer BEPS Pillar Two Readiness Index Report, published in May 2024, that indicates that “70% [of the respondents] still foresee difficulties in data collection and management”. Data, however, is but one of the challenges for companies grappling with the new compliance and reporting requirements of pillar two.

Pillar two challenges

Andy Hung, the director of product management, CCH Integrator, at Wolters Kluwer, identifies several issues for companies attempting to navigate the new tax landscape introduced by pillar two. “Legislative uncertainty is the number one challenge,” he says. “The other major challenge is data collection and data management, and how to operationalise the management of pillar two within the tax function.”

With legislative uncertainty seemingly the number one issue, is there any merit in adopting a ‘wait and see’ stance? Ross Robertson, an international tax partner at BDO, is adamant that such an approach is often based on flawed thinking. “We're seeing a few fairly persistent myths in relation to the application of pillar two, which are contributing to the lack of preparedness with a number of multinationals,” he says.

Robertson believes that many tax practitioners are labouring under the following misconceptions:

Their entities are only in high-tax countries and therefore the rules are not relevant to them;

They will not have any top-up tax, so they do not need to do anything;

They do not have to file a return until 2026, so no action is needed at present; and

Pillar two is a group-level issue and head office will ‘look after it’.

The webinar explains why these beliefs are fallacies and provides a high-level explanation of the following key elements of pillar two:

The income inclusion rule;

Domestic top-up tax;

The undertaxed profits rule;

Domestic minimum top-up tax; and

The subject-to-tax rule.

Pillar two timelines

It is not just tax teams that are scrambling – at least in some cases – to adjust to the pillar two recommendations. Many governments around the world that are intending to apply the measures are striving to enact legislation. On July 5 2024, for example, Singapore closed a public consultation on proposed bills and subsidiary legislation concerning a domestic top-up tax and the income inclusion rule, while HM Revenue and Customs has been sending ‘nudge letters’ to potentially affected organisations in the UK. The clock is ticking for companies and governments alike.

“With all the member countries that have put their hand up saying we'll adopt pillar two, there's no uniformity on the timeline across those OECD countries,” Hung says. “But the effective date for BEPS pillar two is very much right now, with implications for MNEs [multinational enterprises] from 1st January 2024, and if MNEs have not begun to prepare for pillar two, they may fall behind. And the longer it is delayed, the harder it is to get your tax reporting, disclosures, and financial statements in order and on time.”

While there is no uniformity across jurisdictions in terms of a timeline, as indicated in BDO’s implementation status tracker, Robertson emphasises that firms cannot use that as a reason to delay preparation. “Absolutely no time to lose,” he says. “And whilst we've got a model set of rules and principles set out by the OECD, not every jurisdiction is going to follow those model rules and principles to the ‘T’.

“For example, the OECD suggested registration for pillar two should happen six months after the end of the first period when a particular group is in scope. But we've already seen Belgium deviating from that recently by introducing registration obligations at the later of 13th July 2024 or 30 days after the start of the first in-scope period, if that date is later. And Belgium is requiring an awful lot more information on the registration process than the OECD probably envisaged.

“The key point, and we can often lose sight of this when we're talking about pillar two, is it is a tax that is currently in force. There are hundreds of pages of guidance, hundreds of pages of legislation. Then each territory is taking a slightly different approach. I'd really encourage groups to give themselves the time to think through that carefully.”

Safe harbours

A key theme of the discussion concerns the limitations of safe harbours, several of which relate to, again, jurisdictional differences. “You can meet the [safe harbour] test in some territories but not others, in which case you can benefit from the safe harbour in one territory but perhaps not in another,” Robertson says, adding that there is also “a danger around data consistency where data is drawn from different sources for different entities or different jurisdictions that can result in the disqualification of country-by-country [CBC] reports.

I hear, ‘safe harbours’ or ‘I'm going to wait for my adviser to tell me’. That will not be enough

“Also, if you don't qualify in a given jurisdiction for the transitional safe harbour – or indeed don't get into it, even if you do qualify – then if you don't do that in 2024, you cannot rely on the safe harbour for that jurisdiction for 2025 or 2026. So, you really need to make sure that your ducks are in a row for 2024, otherwise you're scuppering your chance for 2025 or 2026, and that's the case even if the entity is in a jurisdiction which the policy rules are not applicable to for 2024.”

Another issue, raised by Hung, concerns potential disparities in the effective tax rate between related entities based in different jurisdictions. “The allocation of additional top-up tax, in theory, should be split between the entities at country level, but if one entity has an effective tax rate of, say, 5% and the other one has it at 20%, meanwhile the country's effective tax rate is 12%, how will one company feel about paying the top-up tax driven by another entity that's been able to have these benefits,” he says. “The complexities are there, but there's also a diplomatic process and we need to start working through the governance infrastructure.”

Even the clear advantage of the safe harbours comes with a caveat. “The big benefit is a reduced compliance burden,” Robertson says. “The calculations are much simplified. But my experience is that not many groups have gone through a diligent assessment of whether their CBC report is qualifying, and I've encouraged groups to do that, because I've yet to find a single CBC process which results in a qualifying CBC report as required by the area rules without some level of adjustment.”

Data gaps

With the safe harbours proving not to be a pillar two panacea, tax technology and its ability to handle complex data-related tasks represents another avenue for tax teams to explore as they search for solutions. “The data is likely to exist across several sources,” Hung says, drawing on his experience of leading a team that works on tax solutions such as CCH Integrator. “To help with that gap analysis, it's important to start with the data you're familiar with that you have, and then work through the mechanics of pillar two. You can work through these with your advisers; you can use software solutions as well to help you.

I've yet to find a single CBC process which results in a qualifying CBC report as required by the area rules without some level of adjustment

“When you work with an off-the-shelf solution that is designed to capture, calculate, and communicate the data and the outputs of BEPS pillar two, it helps you filter through those data gaps. There's no silver bullet on how to capture the data – you know, click the button and it all comes together – [but] I think there are logical and practical steps.”

This quest for a ‘silver bullet’ leads Robertson to take one of his favourite analogies out for a spin. “There's no point having a Lamborghini if you don't know how to drive it,” he says. “The technology is the Lamborghini. Hugely powerful. But the technology can only go so far. Identifying the scope of your group, who are the constituent entities within that, how should those constituent entities be categorised for pillar two purposes… All those points require a human brain to ensure that this technology is set up in the right way. And then you've got various adjustments. There's a huge number of elections within the pillar two rules. Many of these are long term, so there's going to need to be modelling and forecasting, and a human brain applied.

“The solution is the tax team working in conjunction with advisers and the technology to ensure that you take that Lamborghini to your desired destination, and it's not just something fancy for you to show off to your friends.”

Practical steps

Tax functions should ensure their initial inputs make for a comfortable pillar two journey. “First and foremost, you need to understand the scope of application of the rules to your group,” Robertson says. “Then you need to identify the character of each of the constituent entities for pillar two purposes, which impacts how the rules apply and which data points you need to pick up, and how those data points need to be reported. So, depending on whether you're likely to be able to rely on the CBC transitional safe harbour or you're going to need to undertake a full GloBE calculation for a jurisdiction, what are the data points that you're going to need? Which systems? And where are the gaps in that, so you can start to operationalise the process and pull in that data.”

Hung sounds a strong note of caution in his take on how in-scope companies should be preparing and emphasises the importance of establishing governance frameworks in conducting impact assessments. “Work out what your operating model is to manage the BEPS pillar two safe harbours,” he says. “I hear, ‘safe harbours’ or ‘I'm going to wait for my adviser to tell me’. That will not be enough.

“Dust off your tax government framework and policies. This will help you know where to start in managing BEPS pillar two. We can get caught in detail really quickly, but going back to your governance framework and your policies is another area of impact assessment you should be using to guide your decisioning around the management of pillar two.”

The future of BEPS pillar two

With so much on their plate at present, tax teams could be forgiven for not looking at what developments are potentially next on the menu for pillar two. However, Hung and Robertson are keen to offer several theories, including a possible revision of the $750 million global revenue threshold and even process improvements for companies, despite all the challenges.

“MNEs are seeing BEPS pillar two as a trigger to look at process improvement, not just a new compliance or reporting burden,” Hung says. “Information sharing between tax authorities will increase. There's going to be a lot more work within MNEs to ensure they've got the right level of transparency and governance processes in place. Technology will increase over the next two to five years in managing all this and from that, you'll see the skills and resources within tax functions evolve.”

Robertson is also enthused by the potential developments. “It's a fascinating time in international tax,” he says. “When I look at pillar two from a policy perspective, the thing that really jumps out at me is this €750 million global revenue threshold. You've got this arbitrary transition from 749,999,999 to 750 million where you're under a completely different set of tax principles and it creates this two-tier tax system. I think we're likely to see that shift.

“I think we're going to have at least a five-year period of the rules running in the current form and then we may start to see some simplification. It's not beyond the realms of possibility that pillar two becomes the primary basis of taxation in the future. I'm fascinated to see where it goes.”