Cyprus made the headlines recently because of the banking crisis. Irrespective of those problems in the banking sector, Cyprus remains an international business and financial centre continuing to enjoy the same incentives and the existence of more than 48 double tax treaties (DTTs). Its EU membership and compliance with OECD standards, in line with its most favourable tax regime and transparent legal system, places Cyprus among the most favourable holding company destinations.

Cyprus was and will remain a prime venue for the worldwide operations of multinational corporations, having the beneficial corporate income tax (CIT) rate of 12.5%.

Cyprus is also a vehicle for investment for many countries such as Russia, Poland, Ukraine, the Balkans, India and China. It could easily be said that the country functions as a connecting hub for Europe to Central and Eastern European Countries, Asia and the Far East.

Advantages of Cyprus holding companies

The use of Cyprus holding companies is considered a major vehicle for international tax planning for the following reasons:

The provisions of the EU Parent – Subsidiary Directive, as well as Interest and Royalties Directive have full application in Cyprus, resulting in the elimination of withholding tax (WHT) obstacles.

Dividend income received by a company which is a tax resident of Cyprus is exempt from CIT and in most cases is also exempt from the special defence contribution (SDC).

Outgoing dividends paid by the Cyprus company to the ultimate non-resident beneficial owner are exempt from any withholding taxes irrespective of the existence of any DTTs and irrespective of the applicability of the EU Parent – Subsidiary Directive.

Interest income is either taxed under CIT or SDC at the rate of 12.5% or 30% respectively. Where back-to-back loans exist, the 12.5 % tax is levied on the interest spread (on the difference between interest payable and receivable).

The recent amendments to the Income Tax Law provide that 80% of any income generated from IP rights will be exempt from CIT; therefore only 20% of the profits generated from IP rights (royalties) will be subject to CIT at the rate of 12.5%, essentially creating an effective tax rate of 2.5%.

Cyprus provides unilaterally for a tax credit, in the absence of a DTT, for any withholding taxes levied at source in the other country.

Profits from the sale of securities are exempt from taxation in Cyprus. The definition of securities is very broad such as to include ordinary shares, founder's shares, preference shares, bonds and debentures, units in collective investment schemes, options and futures.

The advantages provided by Cypriot holding companies is the main reason for the continuing interest in tax structuring via Cyprus. In the last few months potential investors have attempted to find alternatives to Cyprus tax structuring out of a fear that the beneficial regime will not be maintained. Having found no comparable benefits these investors have decided to continue to use Cypriot tax structures.

The Cypriot financial holding company

Cypriot companies providing certain financial services might need to apply for a Cyprus investment firm (CIF) authorisation from the Cyprus Securities and Exchange Commission (CySec). The CIF authorisation is based on the legal framework which has been transposed in Cypriot law under the EU MIFID Directive.

Do you need to apply for a CIF License?

The first consideration is whether the Cypriot company will be providing and/ or performing investment services. It also does not matter whether the provision or performance of these services is taking place in or outside of Cyprus. The question is what can constitute as investment services for the purposes of the CySec. An illustrative yet not exhaustive list is the following:

Reception and transmission of orders in relation to one or more financial instruments;

Execution of orders on behalf of a client;

Dealing for own account;

Providing investment advice;

Underwriting or any other similar activities of financial instruments; and

Operation of a trading platform.

The second consideration is whether the above mentioned investment services are related to financial instruments. Once again the CySec will mostly look for the following types of financial instruments:

Transferable securities;

Instruments related to the money market;

Units of collective investment undertakings;

Any derivative contracts relating to commodities such as options, futures, swaps, and others that are settled in cash;

Any derivative contracts relating to commodities such as options, futures, swaps and others that can be physically settled and are traded on a regulated market or that are not for commercial purposes; and

Financial contracts for differences.

Should the Cypriot company fall into one (or more) of the categories mentioned under the first and second considerations then the Cypriot company shall need to apply for a CIF licence and thus be regulated by the CySec.

However, subject to conditions, a Cypriot company might obtain an exemption from the obligation of applying for a CIF license.

Advantages of a Cyprus CIF License and structuring ideas

Of course, the most important advantage of choosing to register with a Cypriot CIF, is the advantageous tax regime of Cyprus. With a corporate income tax of 12.5%, no capital gains taxes on the disposal of securities, 0% withholding tax on the payment of dividends to a non-resident shareholder, and of course a wide range of double tax treaties and EU directives.

Registering a Cypriot CIF will allow the provision of financial services anywhere in the EU, or even with the rest of the world, taking advantage of the Cypriot beneficial tax system.

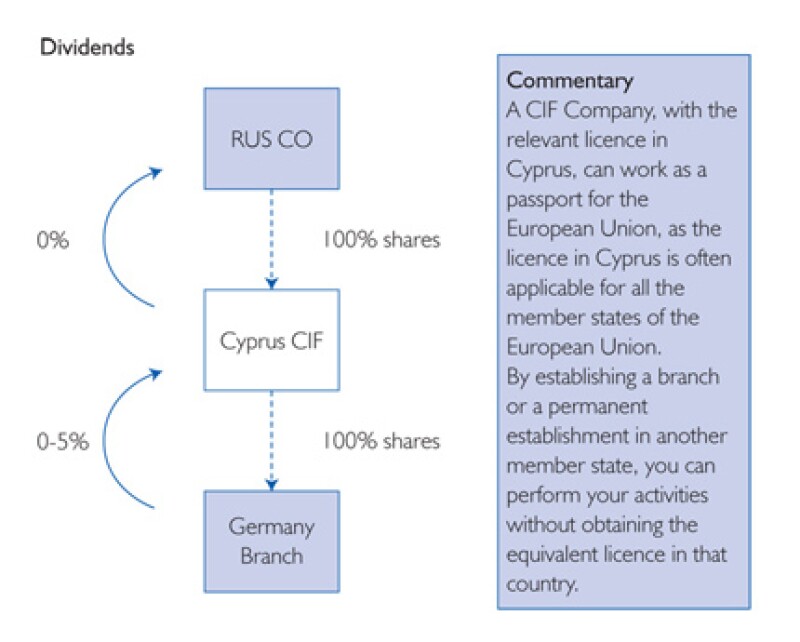

Cyprus legislation (N144(I)/2007 and N106(I)/2009) provide at clause 77 that entities that have obtained such licence in a member state can offer such services in the Republic of Cyprus through a branch or rep office and vice versa, an entity that has obtained a licence in the Republic can perform such services in another member state. A notification must be given and the information of such entity by the relevant authority of the member state of origin.

There are further benefits offered by Cyprus such as an easy-to-do business approach and much flexibility offered by the CySec (see Diagram 1).

Diagram 1: Passport to Europe |

|

It is necessary to provide a few practical examples for potential investors on how a possible Cypriot CIF might obtain its tax benefits.

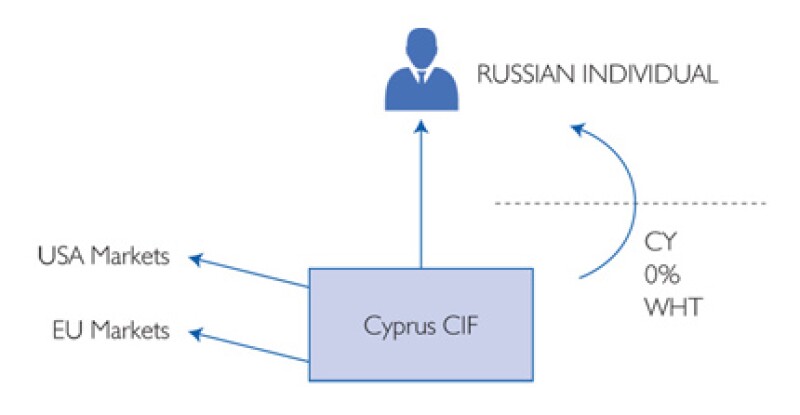

In the example below, a Russian trader decided to use a Cypriot CIF for both its personal dealing activities as well as for providing investment advice and trading on behalf of its clients in the EU and also the US. In its simplest form a possible structure could look like Diagram 2.

Diagram 2: Example 1 CIF |

|

Through the Cypriot CIF, it is possible to trade in foreign markets such as the US and EU and then expatriate gains in the CIF. It is also possible to provide investment advice in the EU. An advantage of the latter is 0% VAT when issuing an invoice to other EU companies. With the many DTTs negotiated by Cyprus you can rest assured that you will be dealing with the most beneficial taxation possible. Furthermore, all gains from own trading or investment advice can be returned as dividends to the Russian owner with a 0% WHT in Cyprus. Similar results can also be achieved with other jurisdictions.

As already explained above, by obtaining the Cyprus CIF passport there is no need to obtain a subsequent licence to trade in the EU. For instance, you can easily be regulated by the CySec and trade anywhere in the EU.

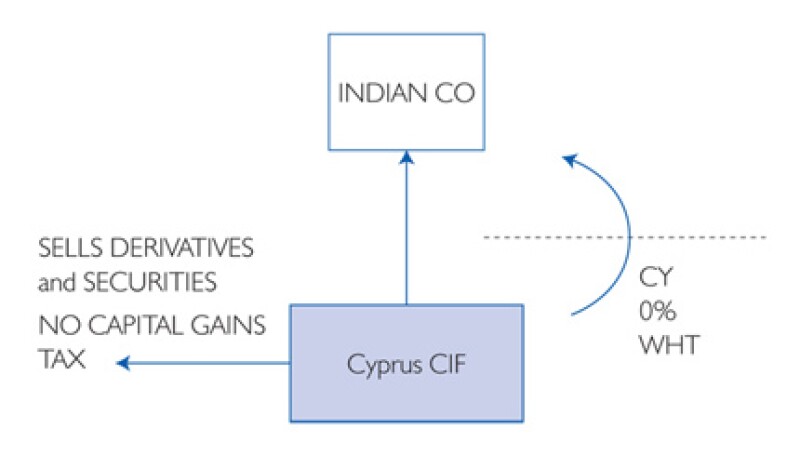

A second example is that of an Indian company selling derivative contracts and listed security titles to the EU (see Diagram 3).

Diagram 3: Example 2 CIF |

|

By selling various EU instruments and securities, and of course having obtained the relevant CIF licence, the Cypriot CIF will not be subjected to capital gains tax. Once again all gains can then be distributed back to the Indian company as dividends with 0% WHT at the level of Cyprus.

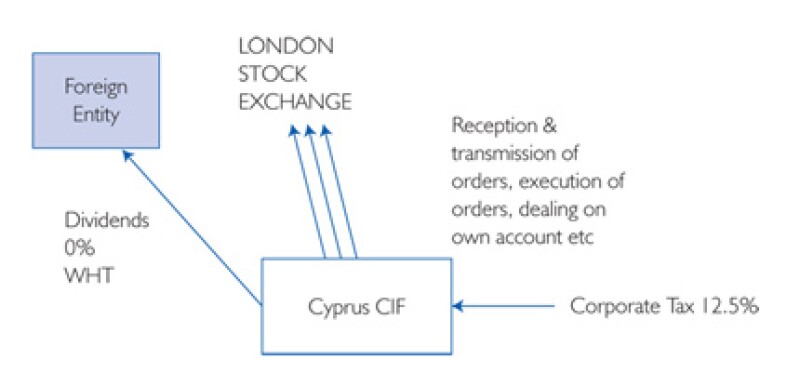

Of course the benefits do not end here. A Cypriot CIF is actually very attractive for investing in the London Stock Exchange (LSE). The main benefit is that by minimising taxation you could have higher returns. In the example illustrated in Diagram 4 below, a Cypriot CIF can be used to trade in the LSE via a variety of methods. All profits can be taxed at the low 12.5% rate and be repatriated accordingly, for example to a foreign entity with low or no tax using the extended DTT network of Cyprus.

Diagram 4: Example 3 CIF |

|

Eurofast's take

The combination of a licensed entity together with the attractive tax regime is a proposition that should be considered. Having also seen the main workings of when and where an application to the CySec is needed, it should be noted that proper advice from a suitably qualified professional should be obtained to determine whether your particular situation or future business plan might need a licence from the CySec. In the situation where it is decided that your Cypriot entity might also need licensing then you should proceed with the necessary application procedure and start trading and/or transacting in the EU or beyond. In cases where a licence is not needed then you shall immediately start enjoying the tax benefits offered by Cyprus and should you decide to visit, enjoy the good weather.

Biography |

||

|

|

Michalis Zambartas Eurofast Taxand Tel: +357 22 699 222 Email: michalis.zambartas@eurofast.eu Website: www.eurofast.eu Michalis Zambartas is a tax and legal associate at Eurofast Taxand. He focuses on international tax planning and international trusts for multinational companies. He also advises on tax-related issues for liquidations, joint ventures, mergers and acquisitions and re-organisations. Michalis has extensive experience in corporate law, in the fields of company law, contract law and maritime law. An indicative list of the clients he advises includes real estate funds, private banks, and high net worth individuals. In addition to his LLB from the University of East Anglia, Michalis has completed an LLM from the University of Wales in Maritime and Commercial Law, as well as an LLM from the University of Lancaster in European and international law. Michalis was admitted in the Cyprus Bar Association in 2004 and is fluent in Greek, English and French. |