Feature

While the IBS incorporates taxable events previously covered by state and municipal taxes, its governance and operational logic represent a significant departure from the legacy model

MNEs now face a shift from modelling to execution as the side‑by‑side deal forces tax teams to upgrade systems, harmonise data, and prevent costly pillar two mismatches

Brazil’s shift to a nationwide consumption tax is more than conceptual; it fundamentally transforms municipal revenue, enforcement, and administrative disputes

As GCCs increasingly become strategic hubs, multinationals face heightened risks around permanent establishment and place of effective management

Sponsored

Sponsored

-

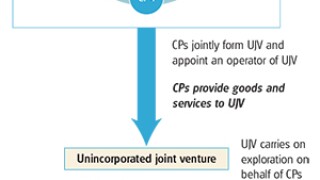

Sponsored by Deloitte Transfer Pricing GlobalIndia’s rapid growth and energy consumption has seen the government simplify public-private investment partnerships in the upstream oil and gas (O&G) sector. Deloitte’s Bhavik Timbadia and Ankit Goel discuss the transfer pricing (TP) implications.

Sponsored by Deloitte Transfer Pricing GlobalIndia’s rapid growth and energy consumption has seen the government simplify public-private investment partnerships in the upstream oil and gas (O&G) sector. Deloitte’s Bhavik Timbadia and Ankit Goel discuss the transfer pricing (TP) implications. -

Sponsored by Deloitte Transfer Pricing GlobalAs resource-rich Middle Eastern governments suffer a decline in oil revenues, many governments are reforming transfer pricing (TP) regulations to limit capital flight. Deloitte’s Shiv Mahalingham, Alena Kovalova and Claire Boushell discuss the regional regulatory trends.

-

Sponsored by Deloitte Transfer Pricing GlobalPublic and political pressure has seen tax authorities play closer attention to transfer pricing. Deloitte’s Tony Anderson, Alex Evans, Mariusz Kazuch, Rafal Sadowski and Lian Tang He explore changes in Canada, China and Poland.

Article list (load more 4 col) current tags