Sponsored

-

Sponsored by Camilleri PreziosiTaxing cryptocurrencies and assets digitally conceived and transferred has little precedence globally. In Malta, the Commissioner for Revenue has recently released guidelines for local authorities to understand their tax liability, particularly as they grow in European popularity. Camilleri Preziosi’s Donald Vella and Kirsten Cassar discuss the VAT, income tax and stamp duty obligations from a Maltese perspective

Sponsored by Camilleri PreziosiTaxing cryptocurrencies and assets digitally conceived and transferred has little precedence globally. In Malta, the Commissioner for Revenue has recently released guidelines for local authorities to understand their tax liability, particularly as they grow in European popularity. Camilleri Preziosi’s Donald Vella and Kirsten Cassar discuss the VAT, income tax and stamp duty obligations from a Maltese perspective -

Sponsored by BurckhardtSwitzerland receives an unprecedented number of information exchange requests every year by foreign countries. Burckhardt Law’s Rolf Wüthrich explores how the private banking state is amending its exchange obligations around share rights and corporate ownership in a bid to harmonise its laws with international norms.

-

Sponsored by Bär & KarrerWithholding taxes are commonly applied in Switzerland to certain debt issues, even though many foreign jurisdictions have abolished such taxes. Bär & Karrer’s Christoph Suter and Susanne Schreiber discuss how Swiss issuers are increasingly limiting their tax exposure through foreign subsidaries and observing lender limits.

-

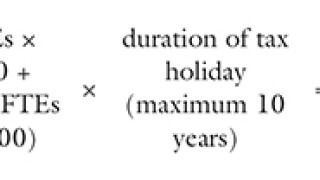

Sponsored by EY SwitzerlandAs Switzerland harmonises its corporate tax regime with international standards, the number of available tax incentives for businesses will diminish, while the effective tax rate will rise. EY Switzerland’s Kersten Honold and Kilian Bürgi discuss how cantonal ‘tax holidays’ provide an alternative to maintain rates below 10%.

-

Sponsored by Deloitte SwitzerlandMost banks make it a policy not to provide tax advisory services, even though there are no regulatory prohibitions to do so in Switzerland, the UK or US. But as tax considerations become increasingly important in any investment strategy, Deloitte Switzerland’s Brandi Caruso and Karim Schubiger discuss the viability of banks providing such an explicit value-add.

-

Sponsored by Lenz & StaehelinSwitzerland has accepted a greater number of exchange of information (EOI) requests from global actors since 2009, harmonising the otherwise private nation’s banking policies with the OECD’s more transparent standards. Lenz & Staehelin’s Jean-Blaise Eckert and Frédéric Neukomm discuss the changes.