The direct tax around which collection revolves in the field of economic activities pursued by legal persons is corporate income tax (CIT).

This tax and personal income tax constitute the foundation for direct taxation in Spain. Both concepts are based on article 31 of the Spanish Constitution, which stipulates that all citizens shall contribute towards the sustenance of public expenditure according to their economic capacity, through a fair tax system inspired by the principles of equality and progressive taxation which may not, under any circumstances, be confiscatory.

Act 43/1995 set out the fundamental rules underpinning CIT in its present form and one of the main developments ushered in by that Act was the determination of the taxable amount based on the book income, as corrected by any available statutory exceptions. Subsequently, to bring greater clarity to the system and increase legal certainty, the Revised CIT Act was approved by means of Legislative Royal Decree 4/2004, on March 5 2004.

The Revised CIT Act has been the subject of constant amendment since 2004 and there has been no comprehensive review of CIT until now. It is at this point in time – having regard to the current economic climate and with the aim of modernising the Spanish economy and raising levels of competitiveness – that Spanish CIT has been reformed. The forthcoming root-and-branch reform of CIT is scheduled to come into force on January 1 2015, and includes important developments regarding the holding regime.

While it is true that the Corporate Income Tax Act 27/2014 overhauls the tax, it is also true that the new CIT carries over the previous tax structure in place since 1996, so that the determination of the taxable amount or tax base hinges on the book income.

This comprehensive review was carried out for, and is underpinned by, the following reasons:

<!--[if !supportLists]-->(i) <!--[endif]-->Simplification of CIT and economic growth:

Simplification of the legislation to promote the growth of small and medium-sized enterprises (SMEs), due to their important position in the Spanish business sector. The aim of this measure is to enhance the ability of Spanish companies to compete in the global marketplace.

<!--[if !supportLists]-->(ii) <!--[endif]-->Increased economic competitiveness and adaptation to EU law:

Membership of a global market, especially within the EU, with the immediate consequence that firms must be able to compete in international markets, in addition to adapting Spanish law to EU law and directing it towards the fight against fraud.

<!--[if !supportLists]-->(iii) <!--[endif]--> Fiscal consolidation and stability of resources:

It must also be noted that the crisis that has hit the collection of this tax, over and above the general financial crisis, has forced lawmakers to react to restore this tax to its rightful place, as a key component of the contribution towards the sustenance of public expenditure.

The most noteworthy developments in the new CIT include: (i) the reduction of the general tax rate (from 30% to 25%, thereby eliminating the difference in tax rate between SMEs and other companies, in line with recommendations from the IMF, which viewed the differential as an obstacle to business growth and productivity. The tax rate for 2015 is 28%); (ii) the withdrawal of certain tax incentives, again with the aim of simplifying the tax; (iii) the introduction of two new incentives to inject capital into companies; (iv) the promotion of other incentives, such as the incentive directed at the film sector; and (v) the review of special CIT regimes, for example the fiscal consolidation regime and the regime applicable to restructuring transactions (such as the tax treatment of merger goodwill).

The holding regime

Analysis of the Spanish holding regime requires looking at the issue in two sub-sections: (i) the tax treatment of income received by the Spanish holding entity (that is, dividends and capital gains); and (ii) the tax treatment of the distribution of income by the Spanish holding entity to its partners. Furthermore, and to flag up the new developments, the future regime will be compared to the current holding regime, which will remain in force until December 31 2014.

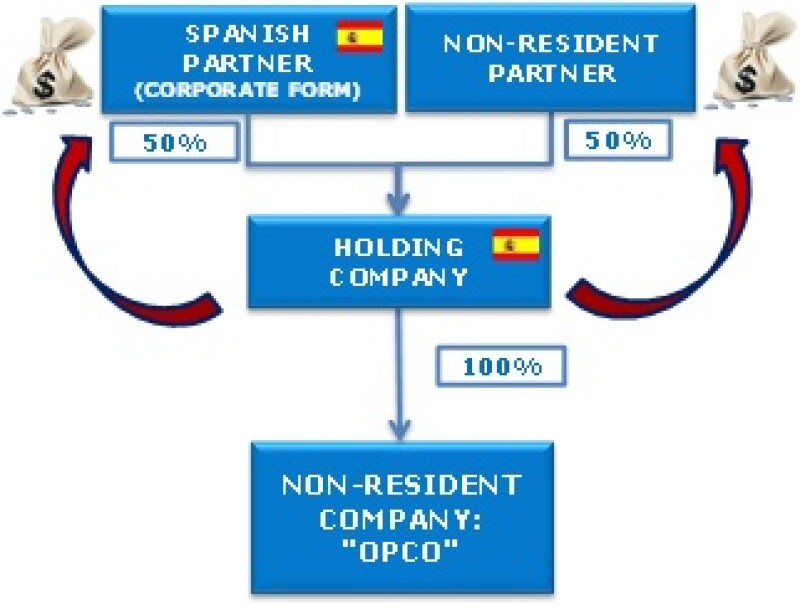

Investment structure

Below you will find a graphical representation of a corporate investment structure with two partners (a Spanish partner and a non-resident partner) in a business pursued by a non-resident operating entity, through a Spanish holding entity.

The holding regime: Tax treatment of income received by the Spanish holding entity.

In this sub-section, I will examine the tax treatment of the income received by the Spanish holding entity (that is, dividends and capital gains). For the purpose of this analysis, the following assumptions have been made: (i) the non-resident entity which pursues the business (Opco) does not reside in a tax haven in accordance with Spanish law; and (ii) the non-resident entity (Opco) is subject to a tax which is similar or analogous to Spanish CIT at a rate of at least 10% (irrespective of the application of any kind of tax exemption, relief, reduction or deduction).

Below you will find a graphical representation of the flow of money, either via dividends or capital gains, from the non-resident entity to the Spanish holding entity:

<!--[endif]-->

Dividends received by the Spanish holding entity as well as any capital gains deriving from the transfer of shares or participations of the non-resident entity are exempt from tax provided that the following requirements are met:

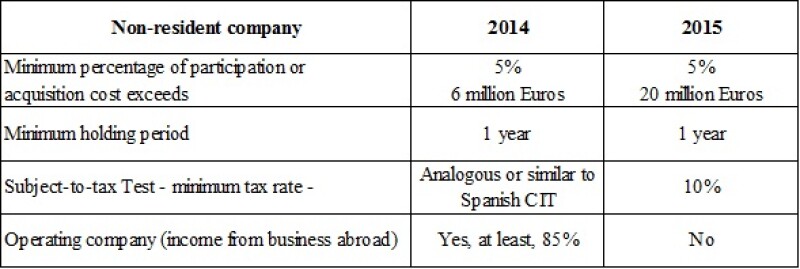

<!--[if !supportLists]-->(a) <!--[endif]-->The direct or indirect percentage participation in the non-resident entity must be at least 5%, unless the cost of acquiring the participation exceeds €20 million, in which case the percentage participation held is not relevant.

Notwithstanding the foregoing, transitional arrangements are put in place for holding entities subject to the ETVE regime (ETVE - Entidades de Tenencia de Valores Extranjeros or Foreign-Securities Holding Entities), which acquired participations during tax periods commencing before January 1 2015. Accordingly, those entities may apply the holding regime in respect of participations in non-resident entities (i) acquired during a tax period commencing before January 1 2015, and (ii) where the acquisition value of those participations exceeds €6 million (naturally assuming, in this case, that the percentage participation does not achieve the minimum requirement of 5%).

<!--[if !supportLists]-->(b) <!--[endif]-->The participation must have been held continuously during the year preceding the date on which the income to be distributed (that is, dividend) becomes due and payable or, failing which, the participation must be held subsequently until that one year period has elapsed. In the case of capital gains deriving from the transfer of shares or participations, this requirement must be met on the date of the transfer.

<!--[if !supportLists]-->(c) <!--[endif]-->The non-resident entity must be subject to, and not exempt from, a foreign tax that is similar or analogous to Spanish CIT at a nominal rate of at least 10% during the tax year in which the income to be distributed or in which a participation is held was obtained. The foregoing is irrespective of the application of any kind of tax exemption, relief or reduction

Please note that the above requirement is deemed to be met if the non-resident subsidiary resides in a tax-treaty country, provided that the corresponding treaty includes an exchange of information clause.

The following table shows the key differences between the existing holding regime and the regime that will apply as from January 1 2015:

As is apparent, one of the main developments is that the income of the non-resident entity need no longer derive from business activities carried out abroad.

The holding regime: Tax treatment of income distributed by the Spanish holding entity to its partners

Let us now turn to the tax treatment of income distributed by the Spanish holding entity (that is, dividends) to its partners or income obtained by those partners from the transfer of shares or participations in that entity (capital gains).

As indicated above, this analysis is based on the same assumptions as those mentioned earlier and, in addition, it has also been assumed that the non-resident partner does not reside in a country or territory which is classified as a tax haven under Spanish law.

Below you will find a graphical representation of the flow of money, either via dividends or capital gains, from the Spanish holding entity to its partners, whether resident in Spain or abroad:

The tax treatment of the income (dividends or capital gains) obtained by the partners of the Spanish holding entity will differ depending on their place of residence for tax purposes.

Regarding the tax treatment of income obtained by the non-resident partner, neither dividends distributed by the Spanish holding entity nor any capital gains deriving from the transfer of shares or participations of that entity are subject to tax in Spain, as these constitute income which is not deemed to be obtained in Spain, provided that the following requirements are met:

<!--[if !supportLists]-->(a) <!--[endif]-->The income that is distributed by the Spanish holding entity corresponds to income which was exempt from Spanish CIT in accordance with the previous sub-section; and

<!--[if !supportLists]-->(b) <!--[endif]-->Any capital gains obtained deriving from the transfer of shares or participations of the Spanish holding entity correspond to (i) reserves recorded out of the exempt income referred to above, or (ii) increases in value attributable to participations in non-resident entities which meet the requirements set out in the previous sub-section.

Second, with respect to the partners of the Spanish holding entity which reside or are established in Spain for tax purposes, a distinction should be drawn between the following types of partner: (a) physical persons; (b) non-residents operating in Spain through a permanent establishment; and (c) legal persons or, in general terms, Spanish CIT payers.

The tax treatment of the income received by each of the above types of partner of the Spanish holding entity is as follows:

<!--[if !supportLists]-->(a) <!--[endif]-->Dividends as well as capital gains obtained by physical persons resident in Spain are classified as savings income and, consequently, are taxable in accordance with the scale established for savings income.

<!--[if !supportLists]-->(b) <!--[endif]-->Non-residents operating in Spain through a permanent establishment and (c) legal persons (in general terms, Spanish CIT payers) may apply the exemption regime set out in the previous sub-section, provided that the necessary requirements are met (that is, minimum participation, holding of the participation, and so on).

One of the main developments in this respect, at least for this author – who had personally endeavoured, without success, to amend the legislation now in force in that regard – is that dividends obtained by physical persons resident in Spain who invest in Spanish holding entities (specifically, ETVEs) will be included in the savings taxable base and not, as has been the case until now, in the general taxable base.