-

Sponsored by Deloitte Transfer Pricing GlobalThe OECD has issued new guidance on applying the profit-split method (PSM) in the energy and resources (E&R) sector. But will this see an uptick in its use? Deloitte’s Mark Barker and Aengus Barry discuss.

Sponsored by Deloitte Transfer Pricing GlobalThe OECD has issued new guidance on applying the profit-split method (PSM) in the energy and resources (E&R) sector. But will this see an uptick in its use? Deloitte’s Mark Barker and Aengus Barry discuss. -

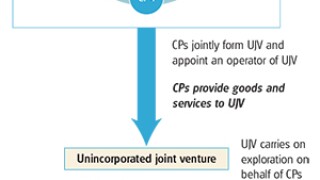

Sponsored by Deloitte Transfer Pricing GlobalIndia’s rapid growth and energy consumption has seen the government simplify public-private investment partnerships in the upstream oil and gas (O&G) sector. Deloitte’s Bhavik Timbadia and Ankit Goel discuss the transfer pricing (TP) implications.

-

Sponsored by Deloitte Transfer Pricing GlobalAs resource-rich Middle Eastern governments suffer a decline in oil revenues, many governments are reforming transfer pricing (TP) regulations to limit capital flight. Deloitte’s Shiv Mahalingham, Alena Kovalova and Claire Boushell discuss the regional regulatory trends.

-

Sponsored by Mattos FilhoGabriela Silva de Lemos explores the conflict between tax authorities and taxplayers as they strive to achieve a balance in concern of tax debt defaults.

-

Sponsored by MachadoBrazil's Federal Revenue Service provided important clarification regarding the concept of inputs for PIS and COFINS credits, but has still left much to discuss.

-

Sponsored by Mattos FilhoBrazil's complex federal and state structure has created a litigious framework for tax authorities, making tax reform in Brazil a continued political focus.

-

Sponsored by Deloitte Transfer Pricing GlobalPublic and political pressure has seen tax authorities play closer attention to transfer pricing. Deloitte’s Tony Anderson, Alex Evans, Mariusz Kazuch, Rafal Sadowski and Lian Tang He explore changes in Canada, China and Poland.

-

Sponsored by Deloitte Transfer Pricing GlobalCross-border cooperation in transfer pricing risk assessments and audits has presented cost saving opportunities, but increased reporting obligations for MNEs. Deloitte’s Manfred Naumann and David Varley explore the experience in Germany and the US.

-

Sponsored by Deloitte Transfer Pricing GlobalDeloitte Touche Tohmatsu’s global transfer pricing practice, in partnership with International Tax Review, is pleased to present the 2019 edition of the Transfer Pricing Controversy Guide, a discussion and overview of the leading issues, challenges and opportunities around transfer pricing (TP) controversy.