Sponsored

-

Sponsored by Deloitte Transfer Pricing GlobalEnergy companies using an asset-backed trading (ABT) model can hedge against volatile markets by better controlling their supply chain, but this can also trigger new transfer pricing issues. Deloitte’s Nick Pearson-Woodd and Marius Basteviken discuss.

Sponsored by Deloitte Transfer Pricing GlobalEnergy companies using an asset-backed trading (ABT) model can hedge against volatile markets by better controlling their supply chain, but this can also trigger new transfer pricing issues. Deloitte’s Nick Pearson-Woodd and Marius Basteviken discuss. -

Sponsored by Deloitte Transfer Pricing GlobalThe OECD has issued new guidance on applying the profit-split method (PSM) in the energy and resources (E&R) sector. But will this see an uptick in its use? Deloitte’s Mark Barker and Aengus Barry discuss.

-

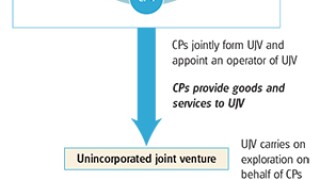

Sponsored by Deloitte Transfer Pricing GlobalIndia’s rapid growth and energy consumption has seen the government simplify public-private investment partnerships in the upstream oil and gas (O&G) sector. Deloitte’s Bhavik Timbadia and Ankit Goel discuss the transfer pricing (TP) implications.

-

Sponsored by Deloitte Transfer Pricing GlobalAs resource-rich Middle Eastern governments suffer a decline in oil revenues, many governments are reforming transfer pricing (TP) regulations to limit capital flight. Deloitte’s Shiv Mahalingham, Alena Kovalova and Claire Boushell discuss the regional regulatory trends.

-

Sponsored by Deloitte Transfer Pricing GlobalEnergy multinationals have complex, international supply chains that contract a host of specialist companies in the process of bringing vital commodities to market, making intellectual property attribution ambiguous. In this primer, Deloitte’s Nick Gaudioso, Randy Price, Nadim Rahman and John Wells give an overview of the energy excavation and production process to understand the tax ramifications.

-

Sponsored by Deloitte Transfer Pricing GlobalAre transfer pricing controversy cases on the rise because of the OECD’s BEPS initiative or local country legislation? Deloitte’s Stan Hales and John Henshall explore the dynamic globally.